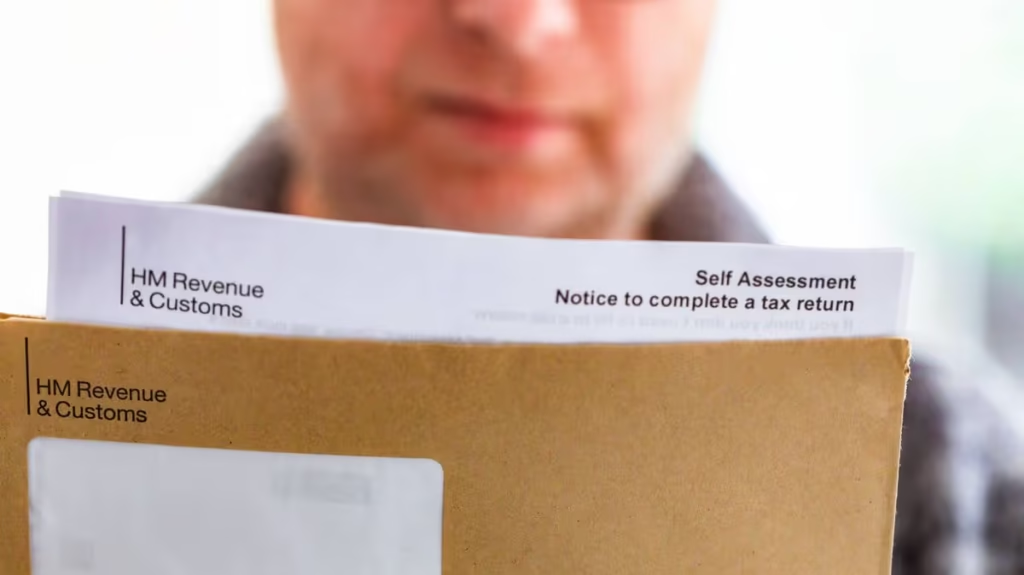

Many UK savers have recently received official correspondence from HM Revenue and Customs regarding their bank interest. These HMRC savings tax letters often come as a surprise, especially after a period of higher interest rates. They inform recipients that their total savings interest may have exceeded the tax-free limit, leading to potential underpaid tax. Understanding these notices helps individuals respond calmly and correctly without unnecessary worry.

HMRC savings tax letters are formal notices sent when banks and building societies report interest earned on savings accounts. The letters explain how much interest HMRC believes you received and whether any additional tax is due. They are not penalties or signs of wrongdoing but part of HMRC’s routine reconciliation process using data automatically shared by financial institutions. Most people receive them because the combined interest from all accounts pushed them over their Personal Savings Allowance.

The Personal Savings Allowance (PSA) allows basic-rate taxpayers to earn up to £1,000 in savings interest tax-free each year. Higher-rate taxpayers get £500, while additional-rate taxpayers receive none. These limits have remained unchanged despite rising interest rates, meaning even modest savings balances can now generate taxable income. Fixed-rate accounts that pay a full year’s interest upfront can quickly trigger these letters, as the entire amount counts in one tax year.

Banks report all savings interest directly to HMRC, which cross-checks it against your PAYE records or previous tax returns. If a mismatch appears, HMRC issues a letter, often called a Simple Assessment or P800, detailing the calculation. The notice may propose collecting the tax by adjusting your tax code for the current year or requesting direct payment. Many recipients with as little as £3,500 in savings have been contacted recently due to the current rate environment.

Receiving an HMRC savings tax letter does not usually require immediate panic. First, verify the details by logging into your Personal Tax Account on GOV.UK and comparing the figures with your own bank statements. Check if the interest amounts are accurate and whether any accounts, such as ISAs, were mistakenly included. If everything matches, HMRC will typically handle collection automatically through your wages or pension.

If the figures seem incorrect, contact HMRC promptly with supporting documents. Common issues include delayed bank reporting, joint accounts, or interest from closed accounts. Responding quickly prevents unnecessary tax code changes or late-payment concerns. Ignoring the letter is not advisable, as it may lead to automatic adjustments that affect your monthly take-home pay.

For those who owe tax, HMRC offers flexible payment options. The amount can be spread through a revised tax code over the year or paid as a lump sum. Some letters allow you to choose the method. Moving future savings into a Cash ISA or Stocks and Shares ISA can protect interest from tax entirely, as ISAs sit outside the Personal Savings Allowance calculation.

Higher interest rates in recent years have caught many savers off guard. Even those who previously stayed well below the allowance now find themselves receiving these notices. Reviewing your overall savings strategy each tax year helps anticipate potential liabilities. Tools on the GOV.UK website and your Personal Tax Account provide estimates based on reported data.

HMRC savings tax letters also serve as a helpful reminder to stay organised. Keep clear records of all accounts, interest statements, and any tax-free wrappers like ISAs. This preparation makes it easier to respond if future letters arrive. For self-employed individuals or those with complex finances, consulting a professional accountant can provide extra clarity.

Understanding these communications empowers savers to manage their finances proactively. The letters reflect HMRC’s improved data-matching capabilities rather than any individual error. By checking details carefully and acting on the guidance provided, most people resolve the matter smoothly.

FAQs

What is an HMRC savings tax letter?

It is an official notice explaining that your reported savings interest may exceed your Personal Savings Allowance, potentially resulting in extra tax due. The letter outlines the calculation and next steps for collection or correction.

Why have I received a letter about savings tax from HMRC?

Banks automatically report interest to HMRC. If the total across all your accounts goes above your allowance, HMRC sends a letter to reconcile any underpaid tax, often due to higher interest rates in recent years.

Do I need to pay tax if I receive an HMRC savings tax letter?

Only if the calculation shows you exceeded your allowance. Review the figures against your statements. If correct, tax will usually be collected via your tax code or a direct payment request.

What should I do after getting an HMRC savings tax letter?

Log into your Personal Tax Account, verify the interest amounts, and respond if the details are wrong. Consider using ISAs for future savings to reduce the chance of similar letters.

Can HMRC savings tax letters be ignored?

It is better not to ignore them. While not urgent penalties, they may lead to automatic tax code adjustments that reduce your take-home pay until resolved.

Conclusion

In summary, HMRC savings tax letters are routine communications designed to ensure correct tax is paid on savings interest that exceeds the Personal Savings Allowance. They arise from automatic data sharing between banks and HMRC and have become more common with elevated interest rates. By carefully checking the information, responding where needed, and planning with tax-efficient options like ISAs, savers can handle these notices confidently. Staying informed about your allowances and maintaining good records helps minimise surprises and supports better financial control in the years ahead.