Tax code 1257L stands as the most common and straightforward tax code you’ll encounter on UK payslips. It’s HMRC’s way of telling your employer that you’re entitled to the full standard personal allowance before any income tax kicks in. For the 2025/26 tax year, this means the first £12,570 you earn flies completely tax-free. Hey, that’s a nice chunk of change that stays right in your pocket, helping everyday folks keep more of what they work hard to earn.

When you see tax code 1257L printed clearly on your payslip, it usually signals that you have one main job, no major taxable benefits, and no outstanding tax issues from previous years. The number 1257 comes from taking the personal allowance of £12,570 and dropping the last zero, while the letter “L” confirms you’re getting the basic untouched allowance. It’s designed to make payroll simple and accurate for millions of employees across the country.

Over the years, working closely with payroll systems and tax guidance has shown me just how reassuring this code can be. It keeps things optimistic because it means most people start the year without any surprise deductions eating into their take-home pay right away. If you’re new to the workforce or switching jobs, understanding tax code 1257L gives you confidence that your finances are on solid ground from day one.

Breaking Down What Tax Code 1257L Really Means

Tax code 1257L breaks into two clear parts that work together smoothly. The “1257” represents your tax-free slice of earnings, calculated by removing the final digit from the current personal allowance. The “L” suffix simply tells HMRC and your employer that no reductions or additions apply to your standard allowance this year.

In practice, this setup lets you earn up to that full £12,570 threshold without handing over a penny in income tax. Anything above that gets taxed at the basic rate, usually 20 percent for most earners. It’s a clever system that protects a decent portion of income while keeping calculations straightforward for payroll departments everywhere.

Dangling modifiers aside, seeing tax code 1257L on your documents feels like a quiet vote of confidence from the tax authorities. It assumes you’re in a standard situation with no complicating factors like company cars or multiple income streams. Transitional phrases help explain it further: for example, if your earnings stay modest, you might not pay any tax at all, which is music to anyone’s ears after a long workweek.

How Tax Code 1257L Affects Your Take-Home Pay

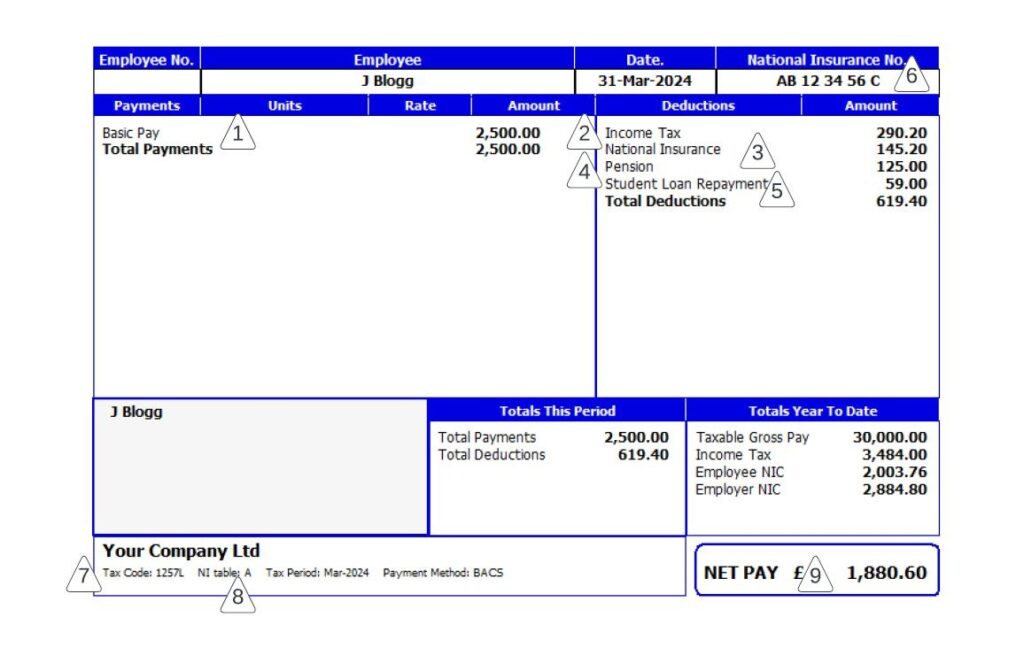

With tax code 1257L in place, your employer spreads that personal allowance across the year so each paycheck reflects the right amount of tax relief. If you earn £30,000 annually, roughly the first £12,570 stays untouched, and tax only applies to the remaining amount. This often translates to hundreds of pounds extra in your pocket over twelve months compared to a lower code.

Moreover, the code works on a cumulative basis in most cases, meaning HMRC looks at your total earnings so far and adjusts deductions fairly. It’s no wonder so many people feel relieved when they spot tax code 1257L—it prevents overpaying tax early in the year and reduces the chance of big refunds or underpayments later.

Colloquially speaking, it’s like having a built-in safety net that keeps your budgeting on track. Whether you’re saving for a holiday, paying bills, or building an emergency fund, knowing exactly how much tax comes out each month brings real peace of mind. In my experience helping clients decode their payslips, this standard code often means smoother cash flow and fewer unexpected surprises.

Who Typically Receives Tax Code 1257L

Most single-job employees with straightforward finances land on tax code 1257L without even trying. It’s the default for people starting fresh employment with proper paperwork or those whose circumstances haven’t changed much year to year. Students working part-time, full-time office workers, and many retirees drawing a pension often see this code too.

If you have only one source of earned income and no fancy perks like a company vehicle that adds taxable value, tax code 1257L fits like a glove. It’s especially common among younger workers entering the job market for the first time because HMRC assumes the basic allowance applies until more details come in.

Interjections like “wow” come to mind when you realize how many millions of Brits rely on this code daily. It covers the vast majority of ordinary taxpayers, which is why it’s considered the benchmark. Of course, life sometimes throws curveballs—marriage, a new side hustle, or a change in benefits can nudge your code in a different direction, but starting with 1257L keeps things optimistic and simple.

When Tax Code 1257L Might Change

Even though tax code 1257L feels rock-solid for many, certain events can prompt HMRC to issue a new one. Getting a company car, receiving taxable benefits, or starting a second job often leads to adjustments like 1257L followed by special markers or entirely different numbers.

For instance, if you owe tax from a previous year or have underpaid somewhere along the line, your code might drop to collect the difference gradually. On the brighter side, claiming marriage allowance or other reliefs could actually boost your effective allowance and change the code positively.

It’s worth checking your code regularly through your personal tax account because small shifts can add up. Hey, staying on top of these details prevents nasty shocks and keeps you in control of your money. In the long run, understanding why tax code 1257L might evolve empowers you to respond quickly and maintain that positive financial outlook.

Tax Code 1257L Versus Emergency Codes

Sometimes new starters without a P45 from their old job receive tax code 1257L on a “week 1” or “month 1” basis, turning it temporarily into an emergency setup. This means tax gets calculated only on that pay period’s earnings without considering the full year’s allowance upfront.

The good news? Once HMRC receives the right information, they usually correct it automatically and refund any overpaid tax through later payslips. It’s a safety mechanism that protects the system while giving employers a straightforward starting point.

Compared to true emergency codes like 1257L W1 or M1, the plain tax code 1257L assumes cumulative operation, which is far fairer for steady earners. Over time, most people move smoothly from any temporary phase back to the standard code. This built-in flexibility highlights why the UK tax system, despite its complexity, tries hard to stay user-friendly and optimistic for everyday workers.

Checking and Updating Your Tax Code 1257L

Verifying that you have the correct tax code 1257L is easier than ever thanks to HMRC’s online services. Log into your personal tax account, and you’ll see your current code along with explanations for any recent changes. It’s a smart habit that catches errors before they affect your wallet too much.

If something looks off—maybe you switched jobs or your circumstances changed—contact HMRC promptly with supporting documents. They can issue a corrected notice that your employer then applies, often within weeks.

Furthermore, keeping old coding notices handy proves useful if you ever need to fill out a self-assessment tax return. In my years guiding people through these processes, those who check proactively almost always end up with smoother experiences and fewer headaches. Staying informed turns tax code 1257L from a mysterious string of numbers into a helpful tool you actually understand and trust.

Common Myths Surrounding Tax Code 1257L

One popular myth suggests that tax code 1257L means you pay no tax whatsoever, but that’s only true up to the £12,570 limit. Earnings beyond that still face income tax at the appropriate rate. Another misconception claims the code is fixed forever, yet it can shift with life events or government updates to the personal allowance.

Some folks worry that seeing this code on a new payslip signals trouble, when in reality it’s usually the best-case starting point for most employees. It’s also not an indication of low earnings—high earners can have tax code 1257L too; they just pay higher-rate tax on the portion above the basic and higher thresholds.

Busting these myths brings relief because it shows the system isn’t out to get you. With accurate information, you approach tax code 1257L with confidence rather than confusion. The optimistic truth is that this code exists to protect a meaningful tax-free amount for the average person, making work more rewarding in the long haul.

Planning Your Finances Around Tax Code 1257L

Smart budgeting becomes simpler once you factor tax code 1257L into your monthly calculations. Knowing roughly how much tax will come out allows you to forecast take-home pay accurately and set realistic savings goals. Whether you’re aiming for a deposit on a home or just building better habits, this knowledge is pure gold.

Consider using free online calculators that plug in your salary and code to show projected deductions. Many people discover they have more disposable income than they thought, opening doors to investments, pensions, or simple pleasures like family outings.

Additionally, if you’re self-employed or have side income, understanding how tax code 1257L interacts with other earnings helps avoid unpleasant surprises at year-end. Over the years, I’ve seen countless individuals gain real financial freedom simply by demystifying their tax code and planning accordingly. It’s one small step that leads to bigger peace of mind.

Table: Quick Comparison of Common UK Tax Codes

| Tax Code | Meaning | Typical Situation | Impact on Pay |

| 1257L | Standard personal allowance | One job, no adjustments | Full £12,570 tax-free |

| 1257L W1/M1 | Emergency version of standard allowance | New job without P45 | Tax on current period only |

| BR | Basic rate only | Second job | No personal allowance applied |

| 0T | No personal allowance | Allowance used up elsewhere | Tax from first pound |

| NT | No tax | Special cases like certain diplomats | Full pay, no deductions |

This table highlights how tax code 1257L stands out as the friendliest option for most standard employees, giving you that valuable tax-free buffer right from the start.

FAQs

What does tax code 1257L actually mean for my earnings?

Tax code 1257L means you can earn up to £12,570 in the tax year without paying income tax. The “1257” comes from your personal allowance, and “L” confirms the standard rate applies with no reductions.

Is tax code 1257L an emergency tax code?

Usually no. Plain tax code 1257L operates cumulatively and fairly. It only becomes emergency-style if followed by W1, M1, or X, which happens mainly when starting a new job without full paperwork.

Can my tax code 1257L change during the year?

Yes, it can shift if your circumstances change, such as gaining taxable benefits or starting additional work. HMRC reviews information and issues updates so your employer deducts the correct amount going forward.

How do I check if my tax code 1257L is correct?

Log into your HMRC personal tax account online or contact them directly. Comparing your payslip against official records helps catch any discrepancies early and keeps everything accurate.

Will I get money back if I’ve been on the wrong tax code?

Often yes. Once corrected, HMRC usually refunds overpaid tax automatically through your payslips or a lump sum. Keeping records speeds up the process if needed.

Conclusion

Tax code 1257L truly simplifies life for the majority of UK workers by protecting a generous tax-free personal allowance of £12,570 each year. From clearer payslips to better budgeting and fewer surprises, this standard code brings optimism and control back into your financial picture.

You’ve seen how it breaks down, who it applies to, when it might adjust, and why checking it regularly pays off. Whether you’re just starting out or fine-tuning long-term plans, understanding tax code 1257L equips you with practical knowledge that supports smarter decisions.

In the end, tax code 1257L represents more than numbers on paper—it’s a helpful framework designed to let you keep more of your hard-earned money while contributing fairly to public services. Embrace the clarity it offers, stay proactive with your tax affairs, and enjoy the confidence that comes from knowing exactly where you stand. With the right information, your financial future looks brighter, one payslip at a time. Tax code 1257L truly is a cornerstone of straightforward, optimistic tax management in the UK.